Is it the death of mid-market? How Zudio, Yousta are reshaping Indian fashion

28 May 2026, Mumbai

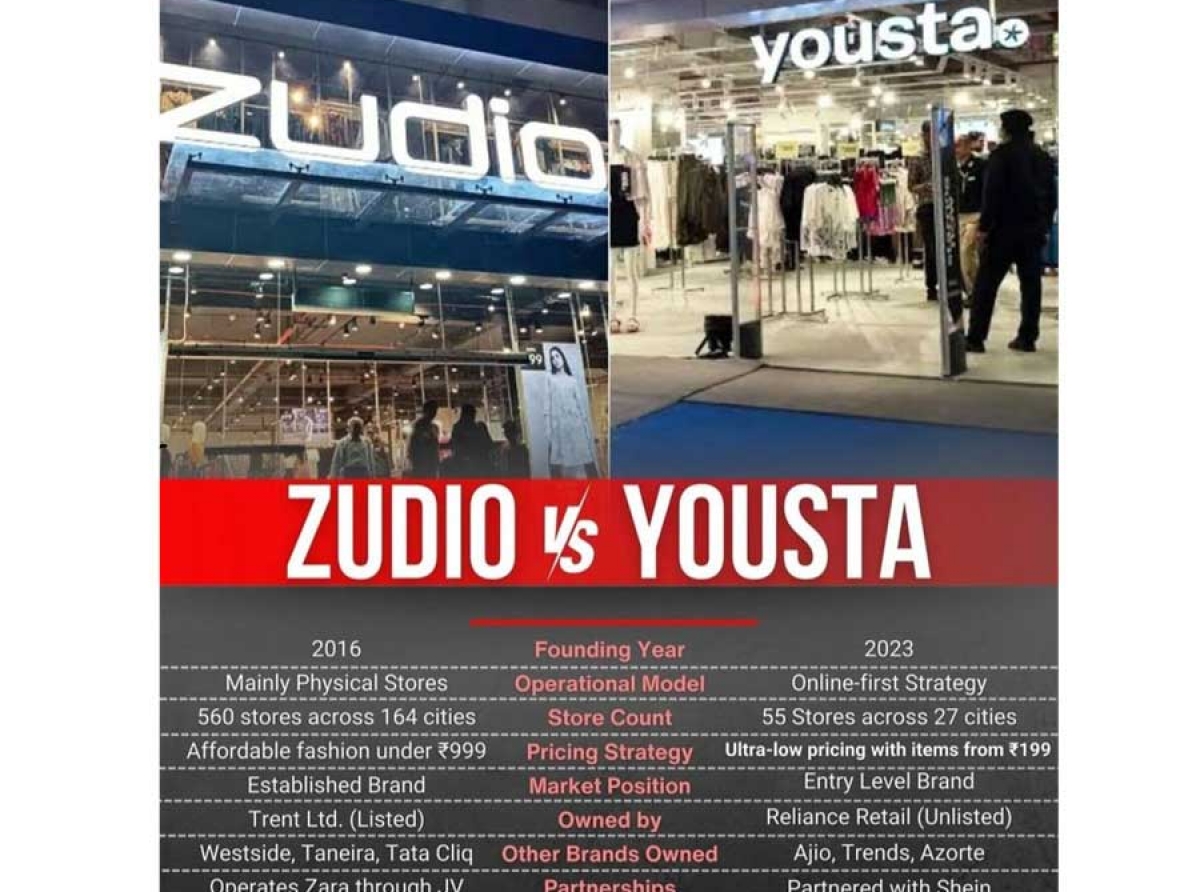

What began as a value-fashion success story led by Trent Limited’s Zudio has rapidly evolved into a wider disruption that is redrawing the economics of fashion retail across the country. By combining ultra-aggressive pricing, vertically integrated sourcing, and rapid inventory turnover, Zudio has effectively altered consumer expectations, particularly among Gen Z and aspirational middle-income shoppers.

The result is a growing crisis for traditional mid-market apparel brands that once dominated the Rs 1,500-3,500 segment. These legacy retailers now find themselves squeezed between premium lifestyle labels at the top and hyper-efficient value chains at the bottom. In this new retail environment, consumers increasingly demand either strong aspirational branding or extreme affordability. Anything in between risks becoming commercially irrelevant.

A new consumer price benchmark

The defining feature of the Zudio model is its rigid pricing discipline. Nearly 90 per cent of its merchandise is priced below Rs 999, creating a psychological ceiling for fashion spending among younger consumers. This strategy has transformed value retail from a discount-driven category into a mainstream consumption habit. The scale of this shift is evident in Trent Limited’s financial performance. The company’s standalone revenue rose 37.4 per cent year-on-year in FY26, with Zudio itself emerging as a billion-dollar revenue engine. More importantly, the format has demonstrated that high-volume fashion retail in India can generate exceptional productivity metrics while operating at low price points.

Industry estimates place Zudio’s revenue per square foot at nearly Rs 16,300, significantly above the broader retail average of Rs 8,000-12,000. Such productivity levels are forcing competitors to reassess long-standing assumptions about margins, inventory, and pricing structures.

For decades, India’s mid-market retailers relied on seasonal discounting, layered distributor networks, and slower inventory cycles to maintain profitability. That model now appears increasingly outdated in an economy where consumers expect trend-led fashion at near-entry-level prices year-round.

Speed becomes the new currency

The rise of value fashion is not simply about cheaper garments. It is fundamentally about operational speed. Zudio’s business model mirrors the fast-fashion mechanics of global giants such as Zara, but at highly localised Indian price points. The retailer’s vertically integrated structure allows it to control design, sourcing, merchandising, and store replenishment with minimal dependency on intermediaries. This eliminates significant costs from the supply chain while enabling faster reaction times to changing fashion trends.

Its inventory refresh cycle reportedly operates at nearly 15 days, compared to the 45-60 day cycle that remains common across much of India’s traditional apparel sector. This velocity allows retailers to continuously introduce new styles, maintain customer excitement, and reduce unsold inventory risks.

The implications for the industry are profound. Fashion retail is no longer merely a battle of branding or aesthetics; it is increasingly a competition of logistics, sourcing agility, and inventory efficiency. Experts say, the Indian consumer has become sharply polarised. Premium shoppers continue to spend on established lifestyle and luxury labels, while value-conscious buyers are prioritising affordability without compromising on trend relevance. Mid-tier brands lacking either differentiation or scale efficiency are finding themselves trapped in the middle.

Corporate India joins the value war

The success of Zudio has led to a broader response from India’s largest retail conglomerates. What initially appeared to be a single-format success has now become the blueprint for a new generation of value-focused fashion chains.

Reliance Retail has rapidly expanded Yousta across more than 200 cities, positioning it as a youth-centric, affordable fashion destination. Aditya Birla Fashion and Retail has increased the rollout of Style Up, while Shoppers Stop has entered the segment through Intune, targeting younger shoppers with low-price trend-led assortments. These launches are not peripheral experiments. They are a decisive shift in retail strategy across corporate India. Unlike older discount-led retail formats that depended heavily on festive sales and end-of-season markdowns, these newer chains operate on an ‘always affordable’ model. Stable pricing reduces dependence on aggressive discounting while protecting margins through tighter inventory control and private-label sourcing. The competitive market now reflects an arms race in efficiency and scale.

Table: The retail competitors

|

Format |

Parent company |

Store count (FY26 est.) |

Price range |

|

Zudio |

Trent (Tata) |

960+ |

Rs 199-999 |

|

Yousta |

Reliance Retail |

200+ |

₹299 - ₹999 |

|

Max Fashion |

Landmark Group |

520+ |

₹499 - ₹1,499 |

|

V-Mart |

V-Mart Retail |

450+ |

₹99 - ₹1,299 |

|

Intune |

Shoppers Stop |

40+ |

₹199 - ₹999 |

Traditional value retailers feel the pressure

The disruption is not limited to mid-market brands alone. Even long-established value retailers are facing pressure to evolve. V-Mart, which built its presence across Tier II and III India through affordable basics and strong rural penetration, is now confronting a younger generation of shoppers seeking both low prices and trend-sensitive merchandise. The arrival of Zudio and Yousta has forced the company to modernise store layouts, improve visual merchandising, and accelerate fashion refresh cycles.

This transition, however, comes with financial strain. Faster inventory turnover and greater design investment compress margins, particularly for retailers accustomed to slower-moving staple products.

Max Fashion shows a similar transformation. Once regarded as the dominant force in organised value retail, Max has repositioned itself toward aspirational fashion and athleisure categories now. Store redesigns, street-style collections, and a sharper Gen Z focus reflect an attempt to differentiate through experience and perceived quality rather than direct price competition. The repositioning highlights a larger industry reality: when ultra-low-price players dominate entry-level fashion, incumbents are forced upward into more premium territory to protect profitability.

The end of the traditional mid-market

Critics argue that the rise of hyper-value fashion risks encouraging lower apparel quality and unsustainable consumption cycles. Yet from a commercial standpoint, the momentum behind the model remains undeniable. India’s fashion industry is bifurcating into two clear segments. On one side are premium and aspirational brands selling lifestyle, exclusivity, and identity. On the other are high-volume value chains built on operational efficiency, rapid replenishment, and accessible pricing.

The traditional mid-market, once sustained through moderate pricing, periodic discounts, and slower fashion cycles is steadily losing relevance. For apparel brands hoping to survive this transition, the challenge extends beyond lowering prices. Success now depends on redesigning supply chains, accelerating product development, strengthening private-label capabilities, and reducing inventory inefficiencies. The Zudio effect is therefore, larger than one retailer’s success. It represents a shift in how Indian consumers define value and how fashion businesses must operate to remain competitive in the country’s next retail era.